Personal Loan Application: Mistakes to Avoid and Common Errors

- Mudra K

- Jun 22, 2025

- 4 min read

📝 Introduction

Getting a personal loan can be a financial lifesaver—whether it's for consolidating debt, covering emergency expenses, or funding a dream wedding. However, applying without preparation can lead to costly mistakes. This article breaks down the most common personal loan application errors, how to avoid them, and how to approach lenders the smart way.

💡 Why Personal Loans Are Popular

Personal loans are unsecured loans, meaning they don’t require collateral. They offer flexibility in usage, fixed interest rates, and manageable monthly payments. However, despite their benefits, many borrowers stumble into traps simply due to lack of awareness or rushing through the process.

⚠️ Common Mistakes in Personal Loan Applications

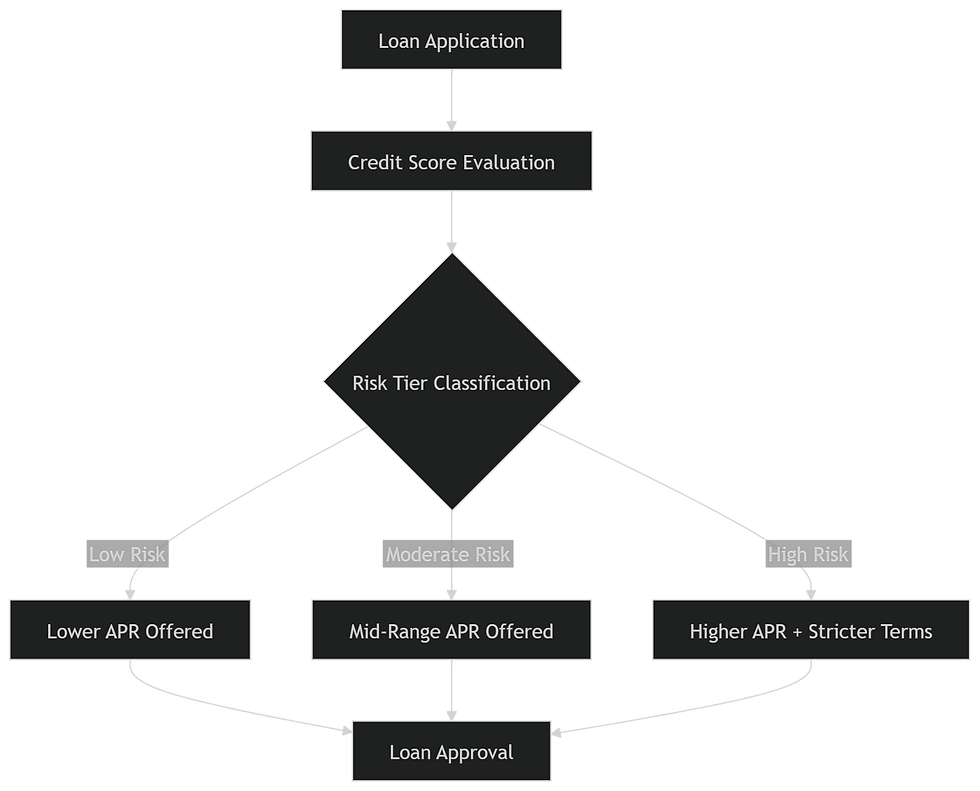

1. Not Checking Credit Score Before Applying

Your credit score is one of the first things lenders check. A low score can mean high interest rates or outright rejection. Always check your credit score beforehand on platforms like CIBIL or Equifax. Please address any discrepancies before applying.

2. Ignoring the Fine Print in Loan Terms

Loan agreements are full of details—interest rate type, processing fees, foreclosure clauses, and late payment penalties. Skipping this can lead to unexpected costs. Always carefully review the fine print and seek clarification if any details are unclear.

3. Borrowing More Than Necessary

It’s tempting to borrow extra “just in case,” but this can lead to unnecessary debt. Please calculate precisely what you need and adhere to that amount. The higher your loan, the more interest you’ll pay over time.

4. Applying with Multiple Lenders Simultaneously

Every time you apply, the lender does a “hard inquiry,” which can dent your credit score. Applying to several lenders at once may look like you're desperate for credit—a red flag for underwriters.

5. Not Comparing Interest Rates and Fees

Don’t jump on the first offer. Compare interest rates, processing fees, and prepayment charges with at least 3–5 lenders. Online marketplaces like BankBazaar and PaisaBazaar can help with comparisons.

6. Misreporting Income or Employment Details

Many applicants overstate income, hoping for better terms. Lenders verify these details, and inconsistencies can lead to rejection. Be honest to maintain credibility and avoid blacklisting.

7. Overlooking the Total Cost of the Loan

Although the EMI may appear low, have you evaluated the total interest paid over the entire loan tenure? Use EMI calculators to assess total repayment and see if shorter tenure makes more sense.

8. Not Considering Repayment Ability

Lenders consider your debt-to-income ratio. Even if approved, you may end up struggling with monthly payments. Ensure your EMI doesn’t exceed 30-40% of your net monthly income.

9. Falling for Pre-approved Loan Traps

Pre-approved doesn’t mean best offer. These are marketing tactics. Please ensure you conduct thorough research before accepting any loan, even if the approval appears to be "instant."

10. Skipping Research on Lenders' Credibility

Not all lenders are equal. Some may have hidden charges, poor customer service, or unreliable digital platforms. Always check lender reviews, licensing, and customer feedback.

📋 How to Correctly Apply for a Personal Loan

✅ Step-by-Step Guide

Check your credit report.

Please assess the exact amount you require.

Research lenders and compare offers.

Gather all required documents.

Please ensure the application is filled out accurately.

Review loan terms before signing.

📄 Documents Required

Document Type | Example |

Identity Proof | Aadhaar Card, PAN Card |

Address Proof | Utility Bills, Passport |

Income Proof | Salary Slips, Bank Statements |

Employment Proof | Offer Letter, ID Card |

📈 Tips to Improve Loan Approval Chances

Maintain a credit score above 750

Limit your existing liabilities

Show stable income and job continuity

Choose a realistic loan amount

Provide accurate and complete documentation

⚖️ Legal and Financial Considerations

Ensure the lender is RBI-registered.

Be cautious of NBFCs or digital lenders offering loans without documentation—some may be illegal.

Keep a copy of the sanction letter and agreement for future reference.

Check foreclosure norms—some lenders charge a fee for early repayment.

❓ FAQs

1. Can I apply for a personal loan with a low credit score?

Yes, but expect higher interest rates or stricter terms. You might want to consider enhancing your credit first.

2. How much personal loan can I get?

It depends on your income, credit history, and existing debts. Most lenders cap at ₹25–₹40 lakhs.

3. Is it safe to apply for a loan online?

Yes, if done through reputable, RBI-registered lenders. Always check for HTTPS encryption and read user reviews.

4. What is the processing time for personal loans?

Typically 1–7 days. Instant loans may be disbursed in hours but often come with higher interest rates.

5. Can I prepay my loan early?

Most lenders allow prepayment but may charge a fee. Check your loan agreement.

6. Will applying multiple times hurt my credit score?

Yes. Too many hard inquiries can lower your score. Apply only when you’re ready with documentation.

🏁 Conclusion

Applying for a personal loan isn’t just about clicking "Apply Now." It’s about smart financial planning, due diligence, and knowing what red flags to watch for. Avoiding common mistakes can help you secure better terms and save thousands in the long run.

Comments