The Surprising Truth: Why Your 800+ Credit Score Isn’t Enough for Loan Approval—5 Secrets Exposed

- Mudra K

- Jun 15, 2025

- 3 min read

Updated: Jun 22, 2025

🧠 The Reality of Loan Rejections Despite Excellent Credit

Imagine this: you’ve hit a personal finance milestone—an 800+ credit score, the mark of financial discipline. However, your loan application may face rejection. Frustrating, right?

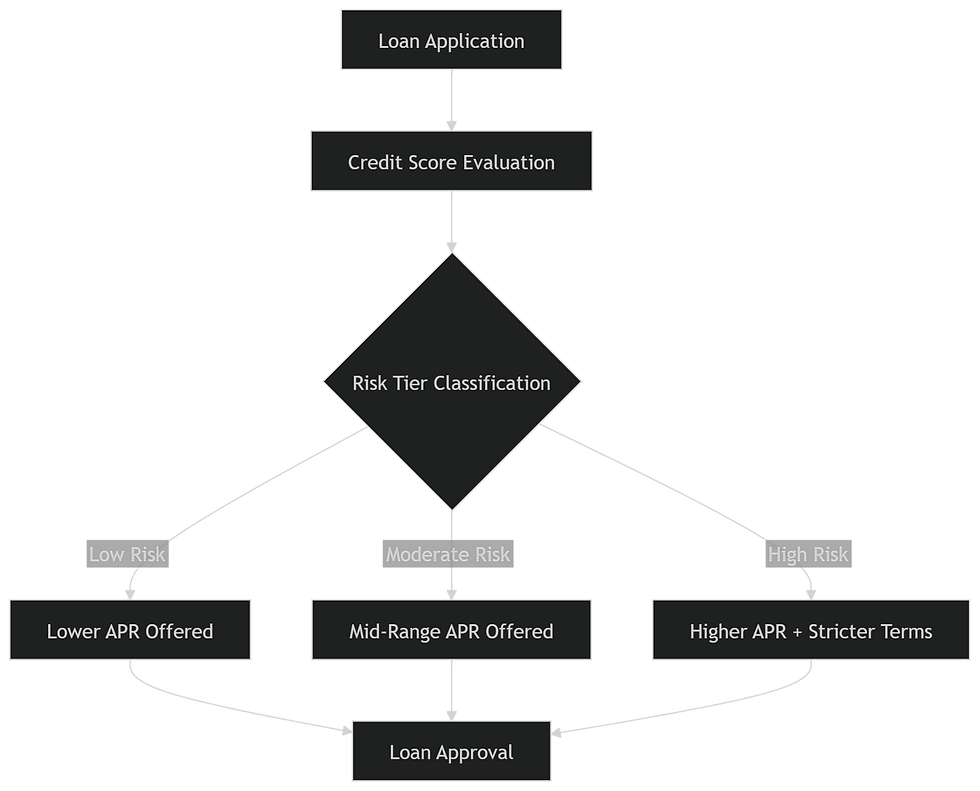

Many people mistakenly believe that having a high credit score guarantees instant approvals. But here's the surprising truth—it’s only one part of a much larger equation. Banks and NBFCs assess a range of factors that could affect your loan eligibility even if your score is excellent.

📊 Please explain the significance of a credit score above 800.?

A credit score above 800 is indeed a stellar achievement. It signals:

Strong repayment history

Low credit utilization

Responsible credit behavior

However, it's important to note that a high credit score solely reflects your past behavior. Lenders want assurance that you can handle future obligations too.

🔍 5 Secrets Behind Loan Rejections With High Credit Scores

Let’s dive into the five surprising reasons why your perfect score might not be enough.

❗ Secret 1 – High Debt-to-Income Ratio (DTI)

Even with a high credit score, if your debt-to-income ratio is above 40–50%, lenders see you as a risk.

What’s DTI? It’s the percentage of your monthly income that goes toward paying debts. A high DTI means there is less disposable income to repay new loans.

✅ Fix Tip: Pay off smaller debts or increase income sources before applying.

💼 Secret 2 – Unstable Employment History

Lenders love stability. If you’ve been

Frequently changing jobs

Recently unemployed

Working on short-term contracts

They might doubt your ability to consistently repay the loan—even if your score is impeccable.

✅ Fix Tip: Show at least 6–12 months of stable income before applying.

📉 Secret 3 – Limited Credit Mix or History

A credit score of 800+ might be based on only one type of credit, like a credit card. Lenders prefer a mix of credit types—revolving (credit cards) and installment (loans).

✅ Fix Tip: Add a secured loan or EMI-based credit to diversify your credit mix.

🧾 Secret 4 – Recent Credit Inquiries

Too many recent credit applications can signal desperation to lenders. Even with a favorable score, if you’ve applied for multiple loans or credit cards recently, lenders may be wary.

✅ Fix Tip: Space out your credit applications and avoid multiple hard inquiries.

💸 Secret 5 – Low Income Relative to Loan Amount

Say you’re applying for a ₹50 lakh home loan but have an annual income of ₹5 lakh—even with an 820 score, it’s likely to be declined.

✅ Fix Tip: Either lower the loan amount or apply with a co-applicant to boost eligibility.

🧾 Why Lenders Look Beyond Credit Scores

A high score doesnot prdoes not complete picture. Here’s why lenders go deeper:

🛡️ Risk Management Perspective

Lenders are more cautious than ever. They evaluate:

Repayment capacity

Cash flow consistency

Credit behavior patterns

A high score is helpful—but context matters more.

📚 Loan Product Guidelines

Each loan product has its own underwriting criteria. Even if you have a high credit score, you may not meet the specific criteria for

Loan-to-value (LTV) ratio

Employment type (salaried vs self-employed)

Age limits or tenure constraints

🔧 How to Strengthen Your Loan Application

A strong credit score plus these enhancements = better approval odds.

📉 Improve Your DTI

Pay off existing EMIs or consolidate high-interest loans. Tools like CRED or Paytm can help track and manage repayments efficiently.

📂 Demonstrate Income Stability

If you’re a freelancer or business owner, keep

IT returns of last 2–3 years

Bank statements

Form 16 or audited financials

🔄 Use a Balanced Credit Portfolio

Mixing credit responsibly shows maturity in credit handling. A combination of

Credit cards

Personal loans

Consumer durable loans

is often more convincing than a single credit line.

🙋 FAQs

1. Can a credit score of 850 still lead to loan rejection?

Yes, if you have high debt levels, inconsistent income, or a mismatch with lender requirements.

2. Is 800+ a favorable credit score in India?

Absolutely! It’s considered excellent. But approval also depends on income, documents, and loan amount.

3. Does changing jobs affect my loan eligibility?

Yes. Frequent changes cause red flags. Lenders prefer 6–12 months in the same job.

4. How many credit inquiries are too many?

More than 2–3 hard inquiries in a short span can hurt your approval chances.

5. What’s a good DTI ratio to maintain?

Keep your debt-to-income ratio below 35–40% for higher chances of approval.

6. Can co-applicants help improve my eligibility?

Definitely. Your loan terms may be improved by a co-applicant who has good credit and a steady income.

✅ Conclusion

While an 800+ credit score is impressive, it doesn't guarantee loan approval. Today’s lenders are looking at the full picture. Factors like DTI, income stability, credit mix, and loan-specific policies heavily influence your application’s outcome.

💡 Pro Tip: Maintain a holistic financial profile, not just afavorabled credit score.

Comments