Jun 83 min read

May 289 min read

USE THIS SPACE TO PROMOTE YOUR BUSINESS

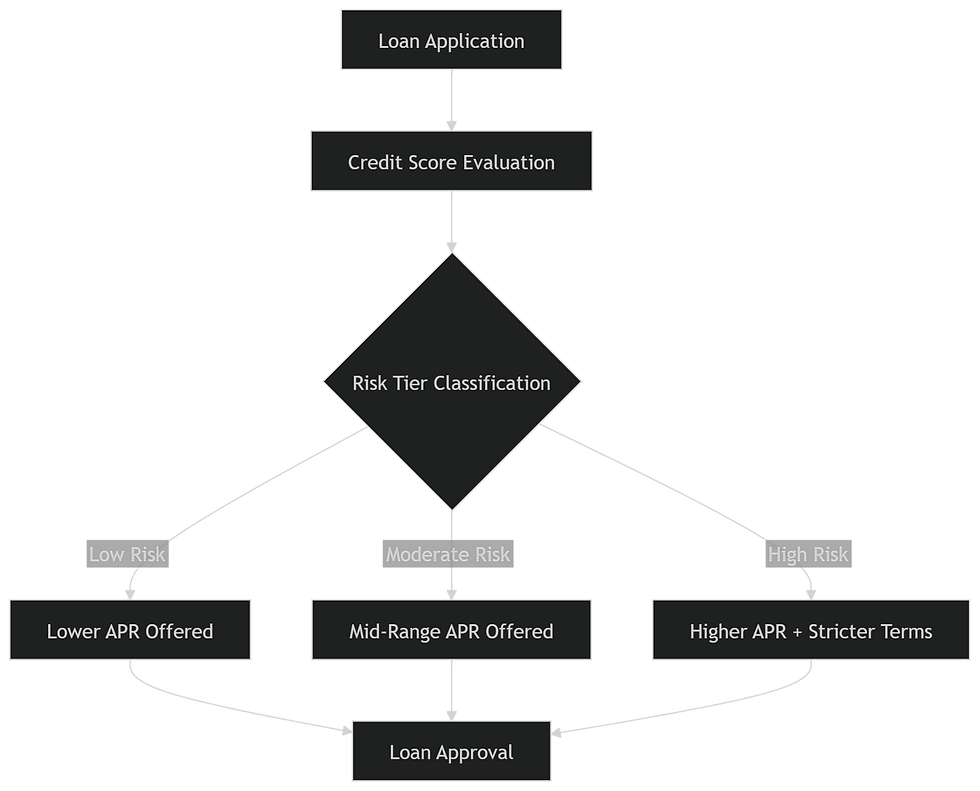

The emergence of fintech has made financial assistance easily accessible. Instant loan apps have revolutionized how individuals access funds, especially during emergencies. These apps offer paperless processes, rapid approvals, and user-friendly platforms, making them a go-to solution for salaried and self-employed users alike.

Benefits of Using Instant Loan Apps

Swift disbursement—Receive funds in your bank account within minutes or hours.

Flexible repayment options—Choose repayment tenures ranging from 3 to 60 months.

Minimal documentation is required; typically, PAN, Aadhaar, and bank statements are sufficient.

No collateral required—most apps offer unsecured personal loans.

24x7 availability—Access loans anytime, anywhere, even on holidays.

These features make instant loan apps a powerful tool for managing short-term financial hurdles.

Flexibility refers to customizable repayment terms, adjustable EMI amounts, and zero prepayment penalties. Here's what you should look for:

Feature | Description |

Tenure Options | Range from 3 months to 5 years |

EMI Customization | Choose EMI dates; adjust based on income |

Foreclosure Charges | Ideally zero or minimal |

Loan Top-Up | Available after timely repayments |

Part-Payment | Ability to pay extra without penalties |

Apps that offer these features empower users to stay in control of their financial health.

KreditBee is one of India's most popular instant loan apps for young salaried individuals and students transitioning into professional roles.

Loan amount: ₹1,000 to ₹400,000

Tenure: 3 to 24 months

Interest rate: 16% to 29.95% p.a.

Eligibility: Indian resident, 21–45 years, salaried

Documents: PAN, Aadhaar, salary slip

Why KreditBee? KreditBee offers low processing fees, instant approval, and direct transfer to bank accounts. Its flexible repayment interface allows for advance EMI payments without charges.

CASHe caters to salaried millennials needing quick short-term loans.

Loan amount: ₹1,000 to ₹400,000

Tenure: 15 to 180 days

Interest rate: ~27% p.a.

USP: Credit scoring via SLQ (Social Loan Quotient)

Special Features:

Fast approval via AI

No CIBIL score required

UPI-based loan disbursement

This loan is ideal for individuals seeking immediate cash for a period of 1 to 6 months, requiring minimal paperwork.

NIRA provides small loans starting at just ₹5,000, making it suitable for first-time borrowers.

Loan range: ₹5,000 to ₹100,000

Interest: From 1.5% per month

Documents: Aadhaar, PAN, Salary slip, Bank statement

Eligibility: ₹12,000+ monthly salary

Why does it stand out? NIRA prioritizes underbanked segments and provides a pre-approved credit line for reuse with timely repayments.

MoneyTap is known for its credit line model—borrow what you need, and pay interest only on what you use.

Credit line: Up to ₹500,000

Tenure: 2 to 36 months

Interest: 13%–24% p.a.

Benefits:

EMI calculator in-app

Flexible EMIs and no usage charges

Real-time loan tracking

This is an intelligent option for individuals who require consistent access to credit, without the need to repeatedly apply.

Dhani gives instant loans based on Aadhaar verification. Do you have a credit score? No problem.

Loan range: ₹1,000 to ₹500,000

Tenure: 3 to 24 months

Specialty: Works for users with low/no credit history

While Dhani offers instant disbursals, it's important to note that interest rates may be higher for no-CIBIL users.

PaySense is popular for salaried and self-employed users alike.

Loan amount: ₹5,000 to ₹500,000

Tenure: 3 to 60 months

EMI: Starts as low as ₹1,000/month

Eligibility: ₹15,000 salary/month

The app features a smart EMI planner, zero prepayment penalty, and easy document upload.

LazyPay offers both BNPL (Buy Now Pay Later) and small personal loans.

Loan size: ₹10,000 to ₹100,000

Usage: Bill payments, e-commerce, utility recharges

Credit limit: Based on mobile number & KYC

LazyPay is ideal for managing regular monthly bills and unexpected expenses alike.

EarlySalary caters to salaried professionals who require immediate cash.

Loan amount: ₹8,000 to ₹500,000

Approval time: Under 10 minutes

Credit score: Not mandatory

It also provides student education loans and wedding loans with customizable tenures.

TrueBalance is a microfinance solution with loans as low as ₹1,000.

Eligibility: Indian citizens with PAN + Aadhaar

Repayment: Via UPI, wallet, or net banking

Interest: 3%–4% per month

Designed for tier-2 & tier-3 city users, TrueBalance supports multilingual access.

Slice offers credit lines with Visa cards, no joining fees, and zero annual charges.

Limit: ₹2,000 to ₹10,00,000

EMI: Up to 36 months

Age: 18+

USP: No hidden charges, app-based KYC

Slice is perfect for students and freelancers, offering a mix of credit card flexibility and loan utility.

When selecting a loan app, evaluate

Interest rate transparency

Ease of repayment

Processing fee

User reviews

RBI-compliant NBFC partners

Use comparison platforms like BankBazaar for informed decisions.

Ensure the app is registered under RBI guidelines

Check for NBFC license details

Read terms carefully—beware of hidden charges

Look for customer support accessibility

Always download apps from the official Play Store or App Store only.

Yes, if you choose apps regulated by the RBI or those partnered with RBI-approved NBFCs. Always review privacy policies.

It varies from 1.5% to 3.5% per month, depending on loan size, tenure, and your credit profile.

Yes. Apps like Dhani, CASHe, and TrueBalance offer loans even with low or no credit history.

The funds typically arrive within 5 minutes to 24 hours following approval and the setup of an e-mandate.

Yes. Most apps now offer zero foreclosure charges, especially those focusing on user-centric experiences.

PAN, Aadhaar, bank statements, and occasionally salary slips or proof of income are required.

These top 10 instant loan apps with flexible repayment options are leading the way in India's booming digital lending space. Whether you're a salaried employee, freelancer, student, or gig worker, there's an app that caters to your specific needs. Always review terms, check user ratings, and ensure you're borrowing responsibly.

Comments