2 days ago3 min read

May 289 min read

Updated: Dec 17, 2024

Choosing between a credit card loan and a personal loan is akin to manoeuvring through a complex financial landscape. Both options promise quick funds when you need them, but each comes with unique features, benefits, and potential pitfalls. So, how do you decide which is the better choice for you? Let’s dive in and untangle this financial puzzle together.

A loan on a credit card is essentially a pre-approved line of credit offered by your credit card issuer. It allows you to borrow up to a certain limit without using your card for purchases. It's quick, convenient, and doesn’t require much paperwork. However, it often comes with higher interest rates.

On the other hand, a personal loan is a sum of money that you borrow from a bank or financial institution. These loans have fixed interest rates, repayment terms, and predictable monthly payments. They’re ideal for larger expenses or planned financial needs.

The main distinctions lie in interest rates, repayment structures, and the borrowing process. Credit card loans are typically easier and faster to access, while personal loans often come with more favourable terms.

Interest rates on credit card loans can soar, often exceeding 18–24% annually. In contrast, personal loans usually have lower interest rates, typically ranging from 10–15%, making them a more cost-effective choice for larger sums.

Credit card loans often entail hidden charges such as processing fees, annual fees, and steep late payment penalties. Personal loans are more transparent, with upfront fees and clear terms. Always read the fine print to avoid unpleasant surprises.

Credit card loans allow you to pay back in smaller, flexible installments. But beware: extending repayment increases interest costs.

Personal loans require you to commit to a fixed repayment period, typically 1–5 years. While this offers predictability, it also demands financial discipline.

Late payments on either loan type can damage your credit score, but the impact is harsher for credit card loans due to higher interest rates compounding over time.

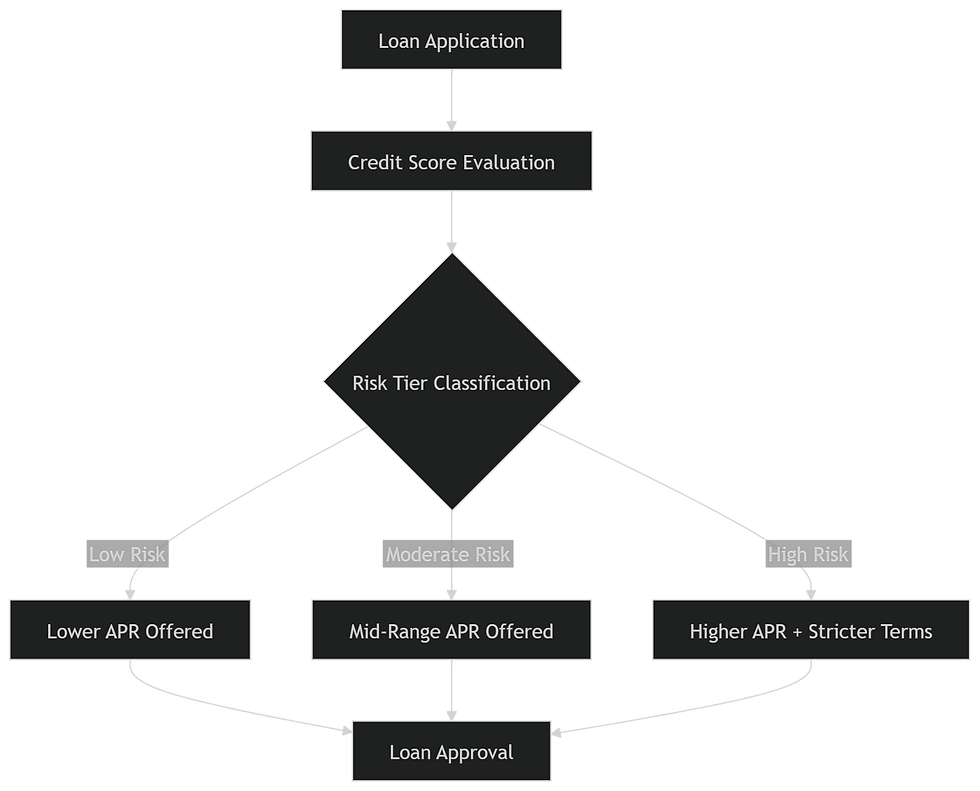

If you have a credit card and a favourable payment history, you’re already halfway there. The approval process is quick, often within minutes.

Personal loans require more documentation, including proof of income and a favourable credit score. While the process is lengthier, the rewards often justify the effort.

Credit card loans win here, as they can be disbursed almost instantly. Personal loans may take a few days to a week.

Emergency medical bills.

Covering short-term cash flow gaps.

Funding higher education.

Home renovation projects.

Pros: Instant access to funds in emergencies without extensive documentation requirements.Cons: High interest rates, hidden fees.

Pros: Lower interest rates, structured repayment.Cons: Lengthy approval process, strict eligibility criteria.

If you need a small sum urgently, a credit card loan might be your go-to. For larger goals, a personal loan is more suitable.

Evaluate your monthly income and existing liabilities. Choose a loan that fits your budget.

Compare interest rates, fees, and repayment terms to make an informed choice.

Deciding between a credit card loan and a personal loan hinges on your unique financial needs and goals. Your financial needs, repayment ability, and long-term goals should guide your decision. Remember, the key is to borrow responsibly and ensure timely repayments to maintain your financial health.

Yes, but ensure you can handle the repayment obligations for both.

Personal loans usually offer better interest rates, making them ideal for consolidating debts.

In some cases, yes. For example, if used for home renovations, you may claim tax benefits.

Yes, it can, especially if you miss payments. Always repay on time to avoid negative impacts, such as damaging your credit score and incurring additional fees.

Maintain a favourable credit score, research lenders, and negotiate terms for the best deal.

Read More: One Credit Score Blogs

Comments