Jun 83 min read

May 289 min read

USE THIS SPACE TO PROMOTE YOUR BUSINESS

Updated: Mar 14

A credit score has become one of the most influential financial indicators in modern lending systems. Whether you want a home loan, a car loan, or even a premium credit card, lenders rely heavily on your credit score to evaluate your financial reliability. In simple terms, a credit score represents how trustworthy you are when it comes to borrowing and repaying money. The higher your score, the more confident lenders feel about offering you credit at favorable interest rates.

In 2026, the importance of credit scores has increased significantly due to rising borrowing costs and stricter lending policies worldwide. Financial institutions are increasingly using sophisticated algorithms and expanded datasets to evaluate borrowers. Even newer financial activities such as Buy Now, Pay Later (BNPL) transactions are starting to influence credit scoring models. This means individuals must be more conscious than ever about maintaining responsible financial habits.

Experts emphasize that credit scores are not static. They fluctuate based on your financial behavior over time. A person who actively manages debt, pays bills on time, and maintains a balanced credit portfolio can steadily improve their credit profile. Conversely, missed payments or excessive borrowing can cause a significant drop in the score.

Understanding how credit scores work is the first step toward improving them. Once you grasp the mechanics behind credit scoring models, you can strategically adopt habits that strengthen your financial credibility and unlock better borrowing opportunities.

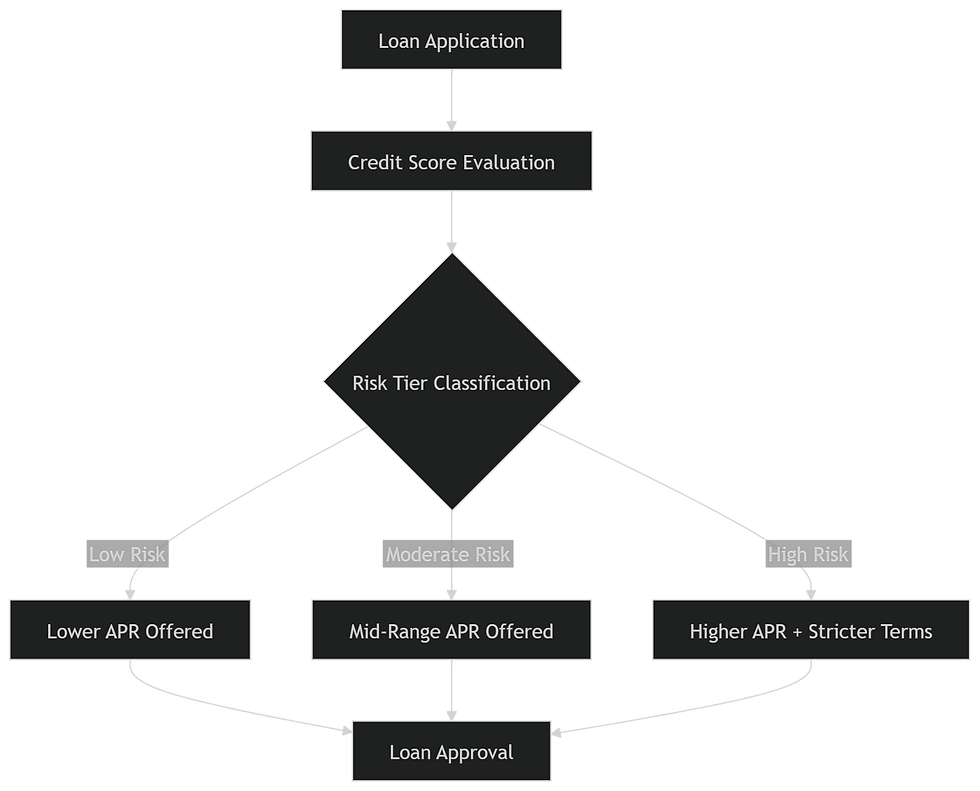

A credit score is a numerical representation of your creditworthiness based on your borrowing and repayment history. Most scoring systems range between 300 and 900 in India, where a score above 700 is generally considered good for loan approvals.

Lenders use this score to assess the risk associated with lending money. A higher score indicates responsible financial behavior, while a lower score suggests potential repayment issues. This simple number can determine whether you receive a loan approval, the interest rate offered, and even the maximum loan amount available.

Credit scores matter because they influence several financial decisions beyond loans. For instance, landlords may review credit reports before approving rental agreements, and employers in certain sectors may also check credit histories when evaluating candidates for financially sensitive roles. In some countries, insurance providers also consider credit-based insurance scores when determining premiums.

The significance of maintaining a strong credit score extends beyond approval rates. Individuals with excellent credit scores often enjoy lower interest rates on mortgages, personal loans, and credit cards. Over the lifetime of a loan, this difference in interest can translate into thousands of dollars saved.

A credit score is essentially a financial reputation scorecard. Just as a strong professional reputation opens career opportunities, a strong credit score unlocks better financial opportunities and greater economic flexibility.

Recent financial trends reveal interesting shifts in global credit behavior. Economic pressures such as inflation, rising interest rates, and increased consumer borrowing have affected credit performance across many regions. For instance, recent reports show that the average credit score in the United States dropped slightly to around 715, reflecting growing financial strain and rising delinquencies.

These trends highlight how external economic factors can influence individual financial health. Higher borrowing costs, increased living expenses, and the return of student loan repayments have contributed to financial stress among borrowers. In response, financial experts emphasize the importance of proactive credit management strategies.

Another notable development is the integration of newer financial behaviors into credit scoring models. The inclusion of BNPL loan activity in certain scoring systems means that smaller installment purchases may now influence a borrower’s credit profile. This shift reflects the evolving nature of consumer finance in the digital age.

For individuals seeking to improve their credit score in 2026, these developments highlight an important lesson: credit management is no longer just about paying loans on time. It also involves understanding emerging financial products, maintaining disciplined spending habits, and staying informed about how credit systems evolve.

By adopting a proactive mindset and monitoring financial activity carefully, borrowers can navigate these changes effectively and maintain a strong credit standing.

Credit scoring systems rely on several key factors to evaluate a borrower’s financial reliability. Understanding these factors allows individuals to identify areas that need improvement and focus their efforts strategically.

Credit Score Factor | Approximate Impact |

Payment History | ~35% |

Credit Utilization | ~30% |

Length of Credit History | ~15% |

Credit Mix | ~10% |

New Credit Inquiries | ~10% |

Payment history and credit utilization are the most influential components of credit scoring models.

These factors collectively create a comprehensive financial profile that lenders use to evaluate risk. A borrower with consistent payment habits, low debt utilization, and a diverse credit portfolio typically receives a higher score.

Each factor contributes to the overall score in different ways, and improving even one area can have a noticeable positive impact over time.

Improving a credit score is not about quick fixes. It requires disciplined financial habits and a clear understanding of how credit systems work. Fortunately, several strategies have consistently proven effective in boosting credit scores over time.

Payment history carries the largest weight in most credit scoring models. Even a single late payment can cause a noticeable decline in your score and remain on your credit report for years.

To avoid this issue, borrowers should prioritize timely payments for all financial obligations, including loan EMIs, credit card bills, and utility payments. Automated payment systems and reminder alerts can be extremely helpful in maintaining consistency.

Financial advisors often describe timely payments as the foundation of a healthy credit profile. When lenders observe a long track record of consistent repayments, they interpret it as evidence of financial discipline and reliability.

Credit utilization refers to the percentage of your available credit limit that you are currently using. Financial experts generally recommend keeping this ratio below 30% to maintain a healthy credit score.

For example, if your credit card limit is ₹1,00,000, your spending should ideally remain below ₹30,000 during a billing cycle. High utilization signals potential financial stress, while low utilization indicates responsible credit management.

Reducing utilization can produce relatively fast improvements in credit scores because this metric updates frequently in credit reports.

Every time you apply for a new loan or credit card, lenders perform a hard inquiry on your credit report. Too many inquiries within a short period can lower your score temporarily because they suggest increased borrowing risk.

Strategic credit applications are therefore essential. Instead of applying for multiple products simultaneously, borrowers should research eligibility criteria carefully and apply only for credit products they are likely to qualify for.

A healthy credit profile typically includes a mix of secured loans (such as home or auto loans) and unsecured credit (such as credit cards or personal loans). Lenders view this balance as evidence that the borrower can manage different types of financial obligations effectively.

Maintaining a diversified credit portfolio demonstrates financial maturity and can contribute positively to your credit score over time.

Some credit improvement strategies can produce noticeable results within a relatively short timeframe.

Being added as an authorized user on a well-managed credit card account can strengthen your credit profile. If the primary cardholder has a strong payment history and low utilization, their positive financial behavior may benefit your credit report.

Increasing your credit limit while maintaining the same spending level automatically reduces your credit utilization ratio. This can improve your score without requiring major lifestyle changes.

Many credit card users fall into the trap of paying only the minimum amount due. However, doing so leads to higher interest costs and slower debt reduction. Paying the full balance each month is a much healthier financial strategy and helps maintain a strong credit profile.

Even financially responsible individuals sometimes make mistakes that negatively impact their credit score.

Missing payments is the most damaging error because it directly affects the most heavily weighted scoring factor. Another common mistake is closing old credit accounts. While it might seem logical to close unused accounts, doing so can shorten your credit history and increase your utilization ratio.

Ignoring errors in credit reports is another serious oversight. Incorrect loan records, duplicate entries, or outdated information can lower your score unnecessarily. Regularly reviewing your credit report and disputing inaccuracies is therefore an essential financial habit.

Credit score improvement is a gradual process rather than an instant transformation. Minor improvements can appear within 30 to 60 days, especially when borrowers reduce their credit utilization or clear outstanding balances.

More substantial improvements often take three to six months of consistent financial discipline. Building a strong credit profile from scratch may take several years, particularly if the individual has limited credit history.

Patience and consistency are the keys to success. Responsible financial behavior over time will eventually be reflected in a higher credit score.

Looking ahead, credit management will likely become even more data-driven as financial technology evolves. Digital lending platforms, AI-based credit models, and expanded financial datasets will shape the future of credit evaluation.

Consumers must therefore focus on building long-term financial habits rather than chasing short-term score improvements. Maintaining low debt levels, tracking expenses carefully, and staying informed about financial products can significantly strengthen financial stability.

A strong credit score is not merely a number—it represents financial trustworthiness. When individuals manage their finances responsibly, they create opportunities for lower borrowing costs, better investment potential, and greater financial independence.

Improving a credit score in 2026 requires a combination of financial discipline, strategic credit management, and awareness of evolving financial systems. Timely payments, low credit utilization, a balanced credit mix, and cautious borrowing habits remain the pillars of a strong credit profile.

By consistently practicing responsible financial behavior and monitoring credit reports regularly, individuals can gradually strengthen their credit standing. Over time, these improvements unlock better loan terms, reduced interest costs, and greater financial opportunities.

The quickest method is to reduce your credit card balances and ensure all payments are made on time. Lowering credit utilization can sometimes improve scores within a month.

Generally, a CIBIL score above 700 is considered good and improves the chances of loan approval.

Financial experts recommend checking your credit report at least once every three to six months to identify errors or suspicious activity.

Not necessarily. Closing an old credit card may shorten your credit history and increase utilization, which can actually reduce your score.

Yes. Responsible use of credit cards, timely bill payments, and maintaining low debt levels can improve your score even without new loans.

Comments