3 days ago9 min read

Personal Loan Interest Rates by Credit Score Explained

- Mudra K

- Feb 28

- 4 min read

The Definitive 2026 Guide to Smarter Borrowing

Understanding personal loan interest rates by credit score is essential when we aim to secure affordable credit and optimise long-term financial outcomes. Lenders price risk with precision, and credit score tiers directly influence the annual percentage rate (APR), approval probability, loan limits, and repayment flexibility. This guide delivers a complete breakdown of how rates are determined, what borrowers can expect across score ranges, and how we can strategically position ourselves for the lowest possible rates.

How Credit Score Determines Personal Loan Interest Rates

Lenders evaluate risk using statistically validated credit models. A higher credit score signals lower default probability, which translates into lower interest rates and better loan terms. Conversely, lower scores trigger higher APRs, stricter conditions, and sometimes reduced loan amounts.

Personal loan pricing typically factors in:

Credit score range

Credit history length

Payment history

Credit utilization ratio

Debt-to-income (DTI) ratio

Recent credit inquiries

Employment stability

Among these, credit score remains the primary pricing variable.

Personal Loan Interest Rates by Credit Score Range (2026 Overview)

Below is a realistic breakdown of average APR ranges based on credit score tiers in 2026:

Credit Score Range | Rating Category | Typical APR Range |

800 – 850 | Exceptional | 5.99% – 8.49% |

740 – 799 | Very Good | 7.49% – 11.99% |

670 – 739 | Good | 10.49% – 17.99% |

580 – 669 | Fair | 18.00% – 26.99% |

300 – 579 | Poor | 27.00% – 36.00%+ |

The difference between a 620 score and a 760 score can result in thousands saved over the life of the loan.

Rate Impact Example: Cost Difference by Credit Tier

Let us consider a ₹500,000 equivalent loan (or $10,000 in USD markets) over 3 years:

At 7% APR → Total interest ≈ significantly lower

At 25% APR, interest cost can nearly triple

Even a 3–5% APR difference materially alters the repayment burden.

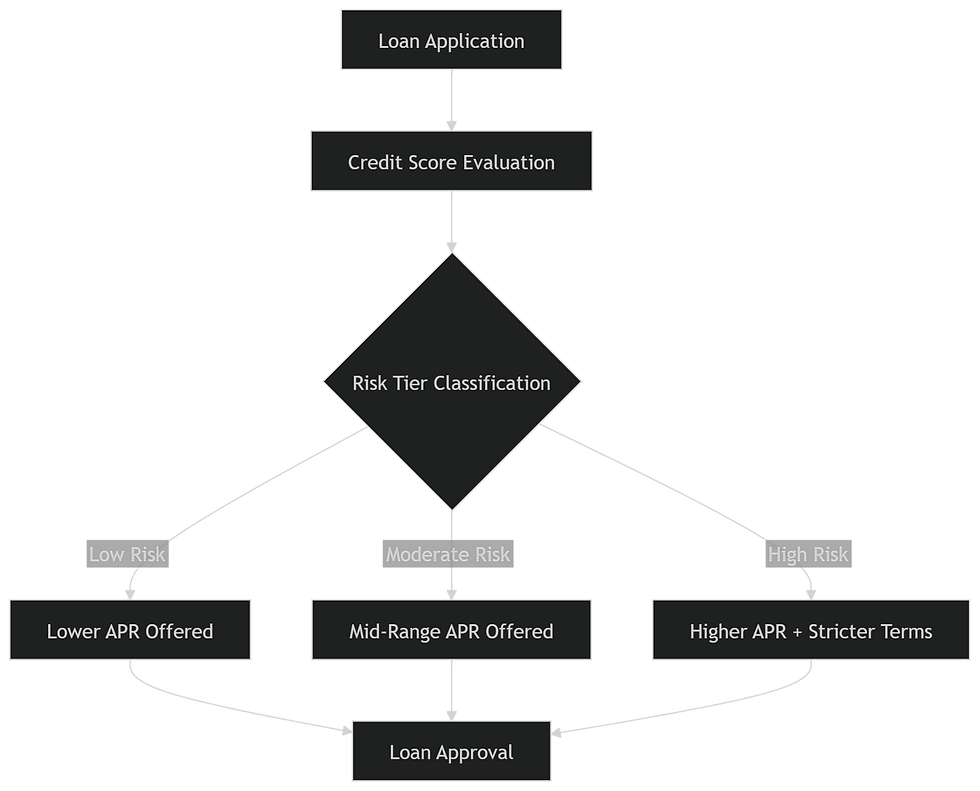

The Risk-Based Pricing Model Explained

Lenders use predictive risk models that estimate default likelihood. The pricing logic follows a structured framework:

flowchart TD

A[Loan Application] --> B[Credit Score Evaluation]

B --> C{Risk Tier Classification}

C -->|Low Risk| D[Lower APR Offered]

C -->|Moderate Risk| E[Mid-Range APR Offered]

C -->|High Risk| F[Higher APR + Stricter Terms]

D --> G[Loan Approval]

E --> G

F --> G

The system ensures rate differentiation aligned with borrower risk category.

Excellent Credit (740+): Securing the Lowest Personal Loan Rates

Borrowers with excellent credit benefit from:

Lowest APR bands

Higher loan limits

Flexible repayment tenures

Minimal origination fees

Fast approvals

At this level, lenders compete aggressively, often offering promotional or relationship-based rate discounts.

Good Credit (670–739): Competitive but Tiered Pricing

We observe that this segment receives strong but not prime-tier rates. Approval likelihood remains high; however:

APR spreads widen

Loan terms may vary

Fee structures become more prominent

Improving a score from 690 to 720 can meaningfully reduce APR offers.

Fair Credit (580–669): Elevated Rates and Structured Conditions

Borrowers in this range face:

Double-digit APRs

Higher origination charges

Lower maximum loan caps

Potential co-signer requirements

Strategic pre-application credit improvement often yields better pricing leverage.

Poor Credit (Below 580): High-Cost Borrowing Environment

Here, personal loans become expensive due to elevated default risk. APRs may approach regulatory caps. Alternative structures such as secured loans or co-signed loans often provide better cost efficiency.

Fixed vs Variable Interest Rates in Personal Loans

Most personal loans offer fixed interest rates, meaning:

Predictable EMI payments

Stable amortization schedule

No exposure to benchmark rate fluctuations

Variable-rate loans may begin lower but can increase depending on market benchmarks.

Debt-to-Income Ratio: The Secondary Pricing Driver

Even with a strong credit score, a high DTI can increase rates. Lenders typically prefer:

DTI below 36% (ideal)

DTI under 43% (maximum tolerance for many lenders)

Lower DTI improves negotiating power.

How Lenders Calculate Final APR

APR incorporates:

Base interest rate

Origination fee

Processing fee

Risk premium

Administrative charges

True cost comparison requires evaluating APR rather than nominal interest rate alone.

Strategies to Qualify for Lower Personal Loan Interest Rates

1. Reduce Credit Utilization Below 30%

Lower revolving balances immediately boost scoring models.

2. Eliminate Late Payments

Consistent on-time payments significantly increase rate eligibility.

3. Avoid Multiple Hard Inquiries

Excessive credit applications suppress score thresholds.

4. Increase Income Stability

Documented stable employment strengthens the underwriting profile.

5. Consider a Co-Signer

A strong co-applicant can substantially reduce APR offers.

Pre-Qualification vs Hard Application: Protecting Your Credit Score

Pre-qualification uses soft enquiries and does not affect credit score. Hard applications can temporarily reduce scores by 5–10 points.

Strategic pre-qualification across lenders allows rate comparison without score damage.

Secured vs Unsecured Personal Loans: Interest Rate Comparison

Loan Type | Collateral Required | Average APR |

Unsecured | No | Higher |

Secured | Yes | Lower |

Secured loans typically offer lower interest rates due to reduced lender risk exposure.

Loan Tenure and Its Impact on Interest Cost

Longer tenure:

Lower monthly payment

Higher total interest cost

Shorter tenure:

Higher EMI

Lower cumulative interest

Balancing cash flow and total cost is critical.

Common Mistakes That Increase Personal Loan Interest Rates

Applying with unstable income

Ignoring credit report errors

Accepting first offer without comparison

Carrying high revolving balances

Choosing excessive tenure

Precision in preparation improves pricing outcomes.

Credit Score Improvement Timeline Before Applying

Action Taken | Estimated Score Impact | Timeline |

Paying down balances | Moderate to High | 30–60 days |

Disputing errors | Variable | 30–90 days |

Removing late payments | High | 3–6 months |

Building payment history | Gradual | 6–12 months |

Even 60 days of preparation can shift rate categories.

When to Apply for a Personal Loan

Optimal timing includes:

After recent score increase

After major debt reduction

During stable employment phase

When market benchmark rates decline

Strategic timing enhances approval and pricing leverage.

Final Perspective on Personal Loan Interest Rates by Credit Score

Personal loan interest rates by credit score reflect measurable borrower risk and pricing algorithms. The difference between tiers is substantial and financially decisive. By optimising credit profile, managing debt ratios, and strategically comparing offers, we position ourselves in the lowest risk category—unlocking competitive APRs, stronger approval odds, and meaningful long-term savings.

Careful preparation transforms borrowing from a costly obligation into a structured financial tool aligned with strategic wealth management objectives.

Comments