Jun 83 min read

May 289 min read

USE THIS SPACE TO PROMOTE YOUR BUSINESS

Updated: Mar 14

An Instant Personal Loan is an unsecured loan that allows borrowers to receive funds quickly—often within minutes or a few hours—through digital applications or online banking platforms. Unlike traditional loans that require extensive paperwork and lengthy approval processes, these loans rely heavily on digital verification systems, automated credit checks, and algorithm-based underwriting models. This technological integration enables lenders to assess risk quickly and disburse funds rapidly to applicants.

The growing demand for instant loans in India reflects changing consumer behavior and the expansion of digital financial services. Individuals frequently seek quick financing for medical emergencies, education expenses, home renovations, travel, or debt consolidation. Because these loans are unsecured—meaning they do not require collateral—lenders depend significantly on credit scores and financial history to evaluate borrowers.

Typically, loan amounts range from ₹10,000 to several lakh rupees, depending on the lender, borrower's income, and credit profile. Interest rates may vary widely, starting around 10.99% per annum with certain lenders, though rates can increase significantly for borrowers with lower credit scores.

An Instant Personal Loan is particularly attractive because of its convenience and accessibility. The entire process—from application to disbursal—can often be completed through a mobile app or online portal. Aadhaar-based KYC, PAN verification, and digital income checks streamline the approval process and reduce paperwork.

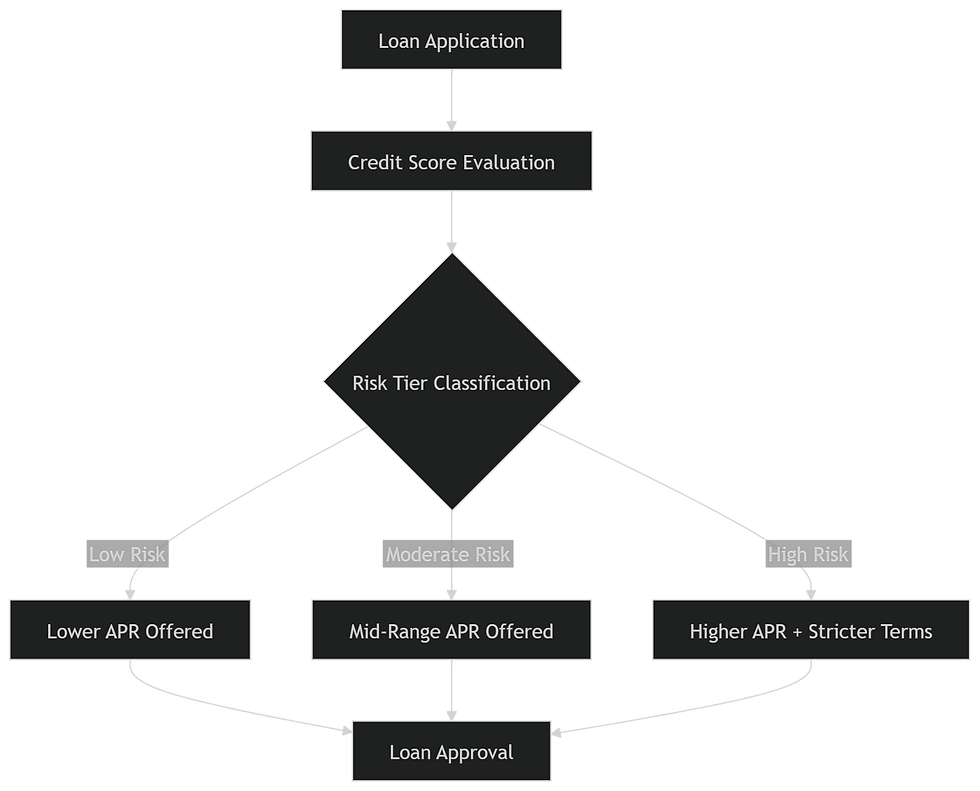

However, while instant loans provide quick access to funds, eligibility criteria remain an important factor. Credit score, income stability, employment history, and existing financial obligations all play a role in determining whether an application will be approved. Among these factors, the CIBIL score remains one of the most influential indicators of creditworthiness.

Instant loans are designed for speed, accessibility, and flexibility. Financial institutions—especially fintech companies and non-banking financial companies (NBFCs)—have leveraged digital infrastructure to transform traditional lending models. The result is a streamlined loan experience that caters to modern consumers who expect fast financial solutions.

One of the defining features of an Instant Personal Loan is its rapid processing time. Traditional bank loans may take several days or even weeks for approval. In contrast, instant loans use automated risk-assessment systems to evaluate creditworthiness in real time. This allows lenders to approve or reject applications almost instantly after submission.

Another important feature is the minimal documentation requirement. Applicants typically need only a few basic documents, such as a PAN card, an Aadhaar card, bank statements, and income proof. Many digital lenders use electronic verification systems to confirm identity and income details, eliminating the need for physical paperwork.

Flexible repayment options also contribute to the popularity of instant loans. Borrowers can select repayment tenures ranging from a few months to several years, depending on the loan amount and lender policies. Some lenders also allow prepayment or foreclosure of loans, enabling borrowers to reduce interest costs.

Despite these advantages, borrowers should be aware that interest rates and fees may be higher for applicants with low credit scores. Because lenders perceive such borrowers as higher risk, they may charge increased interest rates or restrict the loan amount. Understanding how credit scores influence loan eligibility is, therefore, essential before applying.

The CIBIL Score is a three-digit number ranging from 300 to 900 that represents an individual's creditworthiness based on their financial history. This score is calculated by credit bureaus using information such as loan repayments, credit card usage, outstanding debts, and credit inquiries. In India, TransUnion CIBIL is one of the most widely recognized credit information companies responsible for generating these scores.

A higher CIBIL Score indicates responsible financial behavior and a lower risk for lenders. For example, borrowers who consistently repay loans and credit card bills on time typically maintain high credit scores. Conversely, late payments, loan defaults, or excessive credit utilization can reduce the score significantly.

Generally, credit scores are interpreted as follows:

CIBIL Score Range | Credit Category | Loan Approval Chances |

750 – 900 | Excellent | Very high approval chances |

700 – 749 | Good | High approval chances |

650 – 699 | Fair | Moderate approval chances |

600 – 649 | Low | Difficult but possible |

Below 600 | Poor | Very difficult |

Most lenders consider a score above 700 as good, increasing the likelihood of loan approval and favorable interest rates.

The CIBIL Score plays a crucial role in loan decisions because it provides lenders with a quick assessment of financial discipline. Instead of manually reviewing every borrower’s financial history, lenders can rely on this standardized metric to estimate repayment risk.

In the Indian lending ecosystem, most banks prefer borrowers with a CIBIL Score between 700 and 750 or higher. Applicants within this range typically receive quicker approvals, larger loan amounts, and lower interest rates.

However, the minimum required score can vary significantly depending on the lender. Some financial institutions accept applications from borrowers with scores as low as 650, though the terms may be less favorable. (https://www.bajajfinserv.in)

Traditional banks often maintain stricter credit standards compared to NBFCs and fintech lenders. Banks typically prioritize applicants with strong credit profiles because their lending policies emphasize risk minimization. As a result, borrowers with credit scores below 700 may face rejection or receive loan offers with higher interest rates.

Despite these challenges, a lower CIBIL Score does not necessarily mean loan approval is impossible. Certain lenders specialize in providing loans to individuals with fair or even poor credit histories. These lenders use additional evaluation criteria such as income stability, employment record, and banking transactions to determine eligibility.

Understanding these nuances is essential for borrowers seeking an Instant Personal Loan with a credit score below 700. By choosing the right lender and presenting a strong financial profile, applicants can significantly improve their chances of securing quick funding.

Financial institutions operate on risk-based lending principles. In simple terms, lenders evaluate the probability that a borrower will repay a loan on time. When a borrower’s CIBIL Score falls below 700, lenders perceive a higher likelihood of delayed payments or loan default.

This perception arises because credit scores reflect past borrowing behavior. Late payments, high credit card utilization, multiple loan inquiries, or loan settlements can significantly reduce credit scores. From a lender’s perspective, these indicators signal potential repayment challenges.

Because Instant Personal Loans are unsecured, lenders cannot rely on collateral to recover funds in case of default. Instead, they depend heavily on credit scores and income verification to assess repayment capability. If the credit score suggests increased risk, lenders may either reject the application or compensate for the risk by charging higher interest rates.

Another factor influencing loan rejection is regulatory compliance. Financial institutions must maintain healthy asset portfolios and minimize non-performing assets (NPAs). Approving loans for borrowers with weak credit profiles could increase the probability of defaults, affecting the lender’s financial stability.

While the CIBIL Score is important, it is not the only factor lenders consider. Many borrowers mistakenly assume that a low credit score automatically disqualifies them from obtaining an Instant Personal Loan. In reality, lenders evaluate several additional parameters before making a final decision.

Income stability is one of the most critical factors. Borrowers with steady employment and consistent income streams are more likely to receive loan approvals even if their credit score is slightly below the preferred threshold. Lenders assess salary slips, bank statements, and employment history to determine repayment capacity.

Debt-to-income ratio is another key metric. This ratio compares a borrower’s existing loan obligations with their monthly income. If the borrower already has multiple active loans or high credit card balances, lenders may hesitate to approve additional credit.

Other important evaluation criteria include:

Employer reputation

Job stability

Age and professional background

Existing banking relationship

These factors collectively determine whether a borrower qualifies for an Instant Personal Loan, even with a less-than-ideal credit score.

The rise of digital finance has dramatically expanded credit access for borrowers with moderate or low credit scores. NBFCs and fintech lending platforms play a crucial role in this transformation by offering more flexible eligibility criteria compared to traditional banks.

Unlike conventional banks, these lenders use advanced data analytics and alternative credit evaluation models. Instead of relying solely on the CIBIL Score, they analyze additional data points such as mobile usage patterns, digital payment history, and bank transaction behavior.

Many NBFCs offer personal loans even to applicants with credit scores between 600 and 700, although interest rates may be higher due to increased risk.

These lenders often provide quick digital loan approval processes. Applicants can complete the entire application through mobile apps and receive funds within hours after verification.

Borrowers with lower credit scores should expect higher borrowing costs. Because lenders perceive such applicants as higher risk, they adjust interest rates accordingly.

Personal loan interest rates may range from approximately 12% to 30% per annum, depending on credit profile and lender policies.

Higher interest rates serve as a risk-compensation mechanism for lenders. While borrowers with strong credit histories receive preferential rates, those with lower CIBIL Scores must often pay higher EMIs.

Despite the higher cost, instant loans remain valuable for borrowers who require urgent funds. The key is to compare lenders carefully and choose the most affordable option available.

NBFCs typically have more flexible lending criteria than banks. Many specialize in providing loans to borrowers with moderate credit scores or limited credit history. By applying through NBFC platforms, borrowers can significantly improve their chances of securing an Instant Personal Loan even with a score below 700.

Including a co-applicant with a strong credit profile can dramatically increase approval chances. When lenders evaluate joint loan applications, they consider the combined income and creditworthiness of both applicants.

Applying for a smaller loan amount reduces the lender’s risk exposure. Borrowers with lower CIBIL Scores may receive approval more easily for modest loan amounts compared to large loans.

Stable employment and consistent income reassure lenders about repayment capability. Providing salary slips, income tax returns, and bank statements strengthens the application.

Several fintech platforms provide quick Instant Personal Loan approvals through mobile apps. Some lenders even offer credit lines for borrowers with limited credit history.

Feature | Banks | NBFCs / Fintech |

Minimum CIBIL Score | Usually 700–750 | 600–700 possible |

Approval Time | Several days | Minutes to hours |

Interest Rate | Lower | Higher |

Documentation | Extensive | Minimal |

Flexibility | Strict | More flexible |

Borrowers applying for an Instant Personal Loan typically need the following documents:

PAN card

Aadhaar card

Bank statements

Salary slips or income proof

Address proof

Digital verification methods often allow lenders to verify these documents electronically.

Timely repayments significantly improve credit scores. Payment history is one of the most influential factors in credit score calculations.

Keeping credit card usage below 30% of the available limit can positively impact your CIBIL Score.

While Instant Personal Loans provide quick access to funds, borrowers must carefully consider potential risks. Higher interest rates can increase the total cost of borrowing, making repayment more challenging. Additionally, frequent borrowing without proper financial planning may lead to a cycle of debt.

Borrowers should carefully evaluate their repayment capacity before applying for loans. Responsible borrowing practices ensure that loans serve as financial tools rather than long-term financial burdens.

Obtaining an Instant Personal Loan with a CIBIL Score below 700 may seem challenging, but it is far from impossible. While traditional banks often maintain strict credit requirements, NBFCs and fintech lenders have introduced more flexible lending models that expand access to credit.

Borrowers can improve their chances of approval by selecting the right lender, maintaining stable income, applying for smaller loan amounts, or including a co-applicant. At the same time, improving credit scores through responsible financial behavior can significantly enhance future borrowing opportunities.

Ultimately, the key to successful borrowing lies in informed decision-making. By understanding how credit scores influence loan approval and exploring alternative lending options, borrowers can secure the funds they need while maintaining financial stability.

Yes. Some NBFCs and fintech lenders approve loans for applicants with credit scores around 650, though interest rates may be higher.

A CIBIL Score above 700 is generally considered good and increases the likelihood of loan approval with favorable terms.

NBFCs and digital lenders often provide personal loans to borrowers with moderate credit scores.

Yes. Multiple loan inquiries within a short period can negatively impact your credit score.

Some digital lenders approve and disburse loans within a few hours after completing verification.

Comments