What factors affect my personal loan interest rate?

- Mudra K

- Dec 6, 2024

- 2 min read

Various factors influence the interest rate of Personal loan!

Introduction

When considering a personal loan, one of the most crucial aspects is what factors affect my interest rate. The interest rate directly impacts your monthly payments and the overall cost of borrowing. This blog post will explore the various factors that influence personal loan interest rates in India, helping you make informed decisions when applying for a loan.

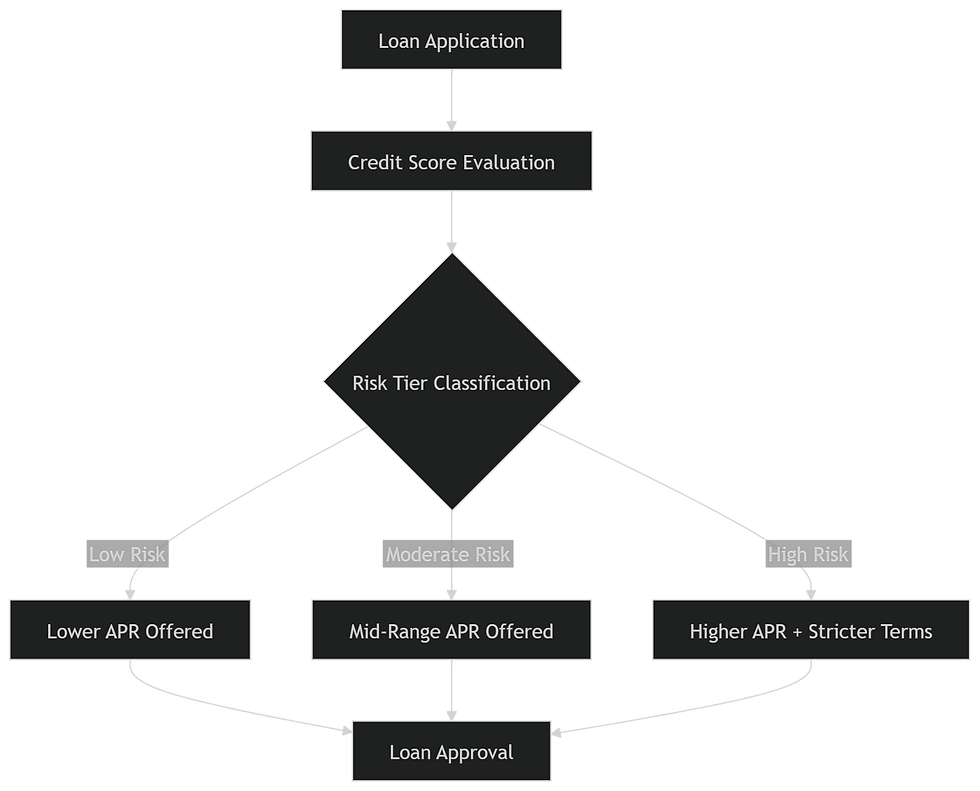

Understanding Personal Loan Interest Rates

Personal loans are unsecured loans that lenders offer based on the borrower's creditworthiness and financial profile. The interest rate on these loans can vary significantly between individuals due to several influencing factors. Understanding these factors can help borrowers negotiate better terms and make smarter financial choices.

Key Factors That Affect Personal Loan Interest Rates

Several key elements determine what factors affect my personal loan interest rate:

1. Credit Score

Your credit score is one of the most significant determinants of your personal loan interest rate. A higher credit score (typically above 700) indicates responsible credit behavior, making you a lower-risk borrower in the eyes of lenders. Conversely, a lower score can lead to higher interest rates or even loan denial.

2. Income Level

Lenders assess your income to determine your ability to repay the loan. Higher-income levels generally lead to lower interest rates, as they indicate better financial health and repayment capacity. For example, a borrower with a stable income of ₹50,000 per month is likely to receive significantly lower interest rates than someone earning ₹20,000.

3. Employment Stability

Job stability plays a crucial role in determining your interest rate. Lenders prefer borrowers with a consistent employment history, as it reflects reliability and financial stability. Frequent job changes or periods of unemployment may raise concerns for lenders, potentially resulting in higher interest rates.

4. Debt-to-Income Ratio

The debt-to-income (DTI) ratio measures your monthly debt payments against your gross monthly income. A lower DTI indicates that you have a manageable level of debt relative to your income, which can positively influence your interest rate. Ideally, lenders prefer a debt-to-income ratio below 35%; higher ratios may result in increased rates due to perceived risk.

5. Macro-Economic Factors

Broader economic conditions also impact personal loan interest rates. Factors such as inflation, the Reserve Bank of India's repo rate, and overall economic growth influence how lenders set their rates. For example, lenders may increase rates when inflation rises to maintain their profit margins and mitigate risk.

Conclusion

In conclusion, understanding what factors affect my personal loan interest rate is vital for anyone considering borrowing in India. Key elements such as credit score, income level, employment stability, debt-to-income ratio, and macroeconomic conditions play significant roles in determining the interest rates lenders offer. By being aware of these factors and improving your financial profile where possible, you can enhance your chances of securing a personal loan with favorable terms and lower interest rates.

Comments